Explore options with our Remortgage Calculator

See your new estimated monthly repayments from your current lender, and the 10 largest UK lenders.

How does the remortgage calculator work?

- Tell us about your current mortgage.

- We’ll check live deals from the 10 largest UK lenders to estimate your new monthly payments.

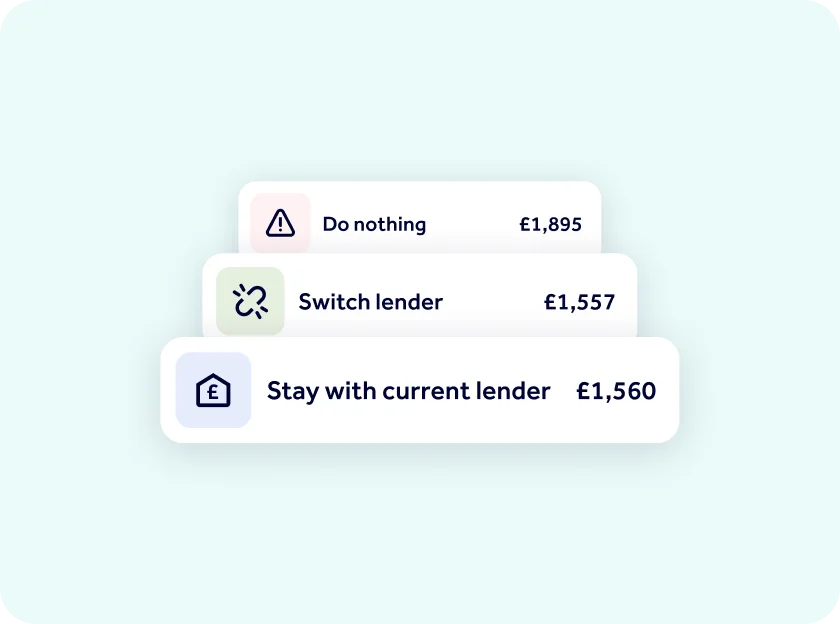

- Compare estimated monthly payments from your current lender, a new lender and your lender’s Standard Variable Rate (SVR).

- To get personalised advice and the best mortgage deal, you can contact one of our broker partners.

The remortgage calculator only works for homes you live in, not for buy-to-let properties.

How reliable are remortgage calculators?

Our remortgage calculator gives you a good starting point for estimating your new monthly payments. It works based on the information you give, so try to make sure it’s as accurate as possible.

We look at deals from the 10 largest UK lenders, which cover 90% of the market. We don’t include shared-ownership deals, and we assume that any product fees will be added to your mortgage. Because we check live deals, the results may change often.

Since we don’t ask about your income, spending, or credit score, the results are just an estimate. For a more personalised result, it’s a good idea to talk to a mortgage broker.

Your questions about remortgaging answered

- Check the current average and lowest UK remortgage rates

- How much can I borrow with a mortgage?

- Check the current UK mortgage rates

- Working out what you can afford when buying a home

- What are the different types of mortgages?

- What are mortgage terms and how do they work?

- How do lenders use your credit score for mortgage applications?

- What's the difference between a hard and soft credit check?

When you remortgage, you'll be applying for a new mortgage for your home from a new lender. If you're switching to a new product with the same lender when your current mortgage deal is ending, this is called a product transfer. Some lenders offer better rates if you already have a mortgage with them, but you may also find a better deal with a new lender so it's a good idea to shop around for the best rate.

It's a good idea to start looking into your options at least 6 months before your current fixed period is due to end.

When you move to a new lender, it's likely you'll have to go through their checks, which means you will need to do a Mortgage in Principle (to check affordability and creditworthiness), provide evidence of your income, have your property valued (although this may not be a physical valuation), and get legal work done by a conveyancer.

If you decide to stay with your existing lender, and don't increase the amount of your mortgage, or the term, you can usually switch online. Your current lender will usually get in touch with you 3-6 months before the end of your deal to outline your options. A mortgage broker can also check if a product transfer is the best option for you, and if so, lock in the rate on your behalf.

If you have a capital repayment mortgage, each payment you've made will reduce the amount that you owe, and your home's value may also have increased. This means when you come to the end of your mortgage deal, it's likely that your Loan-to-Value (LTV) will have gone down, so you'll be able to check if you can access a better mortgage rate, borrow more, or release equity for things like home improvements.

When your current deal is coming to an end, remortgaging will help you to avoid being moved on to a variable rate that is managed by your lender, often called the Standard Variable Rate (SVR). This will usually have a higher rate of interest than the fixed deal you were on previously.

When you remortgage, you'll also have a wider choice of rates by comparing deals across all lenders, which is especially important if you want to borrow more for things like home improvements.

If you stay with your current lender, you may be able to switch to a new deal up to 6 months early, without paying an Early Repayment Charge (ERC). The cost of an ERC is based on the outstanding mortgage amount and how long you have left on your current deal. This is usually a percentage of your outstanding balance and often reduces over time.

Most lenders will also let you cancel a reserved product and move on to another one if rates fall during this period. If you've arranged the remortgage or product transfer yourself, then you'll need to check the market to see if better rates have become available. Whereas if you've used a broker, they will monitor the markets for you. The latest you can change your deal will be about a few weeks before your current rate ends, after this point it will be more difficult to change products. It's best to check with the lender, or your broker, to understand how this process works.

When you remortgage to a new lender, you'll be making a new mortgage application. The amount you can borrow is determined by an affordability assessment and credit check. This is because when you buy a home, the lender will have rules and policies that are set around the Loan-to-Value (LTV), which reflects the size of the mortgage loan you need as a proportion of the value of the home you want to buy.

You can apply direct with a lender for a remortgage, or speak to a mortgage broker, who will help you to work out how much you can borrow and what sort of mortgage to take out. They'll talk through your specific circumstances to help determine the best lender and deal for you.

When you look for a mortgage deal, you'll be asked to answer questions about your current circumstances. Things like if you're coming to the end of your current deal, or if you're buying a new home. And if you're looking to stay with your existing lender or move to a new lender.

Your answer will determine the range of rates you'll be shown as mortgage deals vary. You can use our Remortgage Calculator to check the latest deals from the 10 largest lenders in the UK, as well as your current lender, and we'll also show you the cheapest deal available.

Check the current UK remortgage rates here.

When you remortgage with a new lender, you'll be making a new mortgage application. The amount you can borrow with a mortgage is determined by an affordability assessment, which includes reviewing your monthly income and outgoings, and anyone else's your applying with. They will also do a credit check and review the value of your property.

If you decide to stay with your existing lender, and don't increase the amount of your mortgage, the process of switching is usually a lot easier and cheaper, and it can often be done online. Because you're staying with your existing lender, there's no conveyancing costs, no property valuation and no affordability checks, such as a credit check.