October 2024

Strong activity but muted Autumn price bounce as buyer choice builds

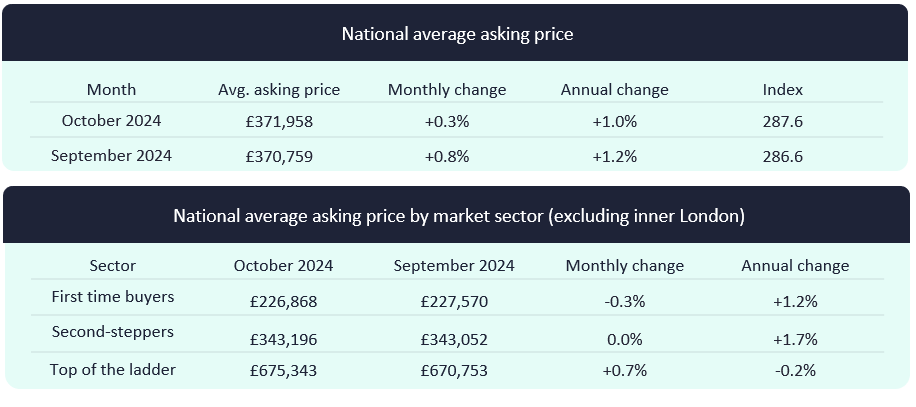

- Average new seller asking prices rise by just 0.3% (+£1,199) this month to £371,958. This is much lower than the average seasonal 1.3% monthly increase at this time of year

- Market activity remains strong, but the muted Autumn price increase comes as buyer choice and seller competition rise:

- The number of sales being agreed is up by 29% year-on-year, a strong rebound from the weaker market a year ago

- Underlying buyer demand remains strong, with the number of people contacting agents about homes for sale up by 17% compared with this time last year, despite some uncertainty caused by the Autumn Budget

- The number of available homes for sale is 12% higher than a year ago – and the highest per estate agent since 2014, intensifying competition to find affordability-stretched buyers, some of whom may also have pre-Budget jitters

- The outlook remains positive for 2025, but affordability pressures remain, and some buyers may be waiting for Budget clarity and cheaper mortgage rates before acting:

- The average 5-year fixed mortgage rate is now 4.61%, up from 4.55% last week, the first weekly increase since May

- The average annual energy bill for a home with an EPC rating of D is £2,465, up by 10% since September

- Financial markets are still predicting two Bank Rate cuts before the end of the year. Combined with wage growth currently outpacing house price growth, which is also boosting affordability, this suggests an active 2025

The average price of property coming to the market for sale rises by 0.3% this month (+£1,199) to £371,958. This is a much lower monthly increase in new seller asking prices than is typical at this time of year, with the long-term average October rise being +1.3%. This much more muted than usual Autumn price bounce comes as buyer choice increases to a level not seen for ten years, putting downwards pressure on price growth. With a greater choice of properties to consider, buyers are making use of their increased negotiating power, helping to keep price rises subdued. However, market activity remains strong despite some uncertainty created by the upcoming Autumn Budget. This month’s limited price growth is also in part down to some sellers heeding agents’ and Rightmove’s caution to price attractively to find a buyer, particularly with seller competition rising, helping to keep activity moving. Affordability remains stretched, limiting buyers’ purchasing power, but there are encouraging signs of this improving next year.

“This month’s subdued price growth, comes as buyer choice soars to a level not seen since 2014. With the ball in the buyer’s court and the pick of a big crop to choose from, sellers need to be pricing competitively to find a buyer, particularly with affordability still very stretched. Some sellers appear to be acting on this caution, contributing to limited price growth and better buyer affordability. This is helping to keep the number of sales being agreed consistently and strongly ahead of the quieter market of this time last year. We’re not seeing activity slow down, but some estate agents report that some movers are now waiting for Budget clarity and anticipated cheaper mortgage rates later this year. However, others state that movers are largely just getting on with plans.”

Tim Bannister Rightmove’s Director of Property Science

The latest snapshot of sales activity shows that the number of sales being agreed is now 29% ahead of the same period last year. Therefore, sales activity has not only bounced back from the low of last year but has continued on an upward trajectory. There is also a healthy level of underlying buyer demand as people continue to plan their next move. The number of people contacting agents about homes for sale is up by 17% compared with this time last year.

However, despite this strong housing market activity, the number of new properties coming to the market, and the time they are taking to sell are both increasing, resulting in an increase in available homes for sale. This reflects that some aspiring buyers are still priced out of the market . The number of available homes for sale is 12% higher than at this time last year, but also the average number of homes for sale per estate agent branch is at its highest since 2014. Competition for buyers is particularly intense at the top-end of the market, where the number of four-bedroom detached houses and five-bedroom-plus homes available for sale is 17% ahead of last year. It’s a buyer’s market, reinforcing the need for sellers to price competitively while affordability is stretched and choice is high.

After a long run of mortgage rate drops helped by the August Bank Rate cut, rate falls are stalling for the moment against a backdrop of geopolitical tension. The average 5-year fixed mortgage rate is now 4.61%, up slightly from 4.55% last week, the first weekly increase since May. Though this is still a big improvement from the average of 6.11% at the peak in July 2023, and is only a very slight increase, the upward swing in rates may be a dent to home-buyer confidence. Rightmove’s Energy Bills Tracker also highlights the impact that rising energy prices are having on household finances. As an example, the average annual energy bill for a home with the typical Energy Performance Certificate (EPC) rating of D, is £2,465, up by 10% or £224 compared to September due to the price cap increase at the start of this month.

Despite these affordability pressures, there are positive signs for 2025. The financial markets are still predicting two Bank Rate cuts before the end of the year. If these go ahead, it is expected that further mortgage rate cuts should follow. While mortgage rates are not expected to return to the ultra-low levels of recent years, further drops when combined with wage rises and muted house price growth would be a big step forward for home-buyer affordability.

“Despite a Budget-shaped cloud on the horizon, the big picture still looks positive for the market heading into 2025. Market activity remains strong, despite affordability pressures on movers. Once we have more certainty about the contents of the Budget, hopefully followed by speedy second and third Bank Rate cuts, we could see another surge in market optimism like we had in the Summer. Affordability is still the biggest barrier facing many movers, with mortgage rates still high, so if the expected two cuts come to fruition it could be the boost that many buyers-in-waiting need. 2025 could see the return of the previously priced out buyer.”

Tim Bannister Rightmove’s Director of Property Science

Experts’ Views

“Activity has been strong; we’ve seen a surge of new instructions in September and is one of our busiest months for new sellers in the last decade. We’ve also seen a good jump in new potential buyers, as well as agreed sales in the area, so it’s been busy. The Bank Rate cut and lower mortgage rates definitely played their part in helping more people to come to market. There’s always some uncertainty surrounding the Budget, but we’re not seeing any buyer hesitation due to it. Despite some mortgage interest rates trickling upwards, the changes are small and not of major concern right now.”

Chris Rowson, Managing Director of Sharman Quinney in Peterborough

“We’ve seen one of the best years for number of transactions in our 18-year history and while activity has been exceptional, price growth has been muted. This could be down to the ‘new normal’ of higher interest rates but also a particularly steep increase in values post-pandemic which will need more time to level off. Moving into the new year we were expecting a pre-election pause, but did not expect a second hiatus due to the new government’s much anticipated first budget. However, we’re hoping for a good end to the year once this pause button is released.”

Joel Baseley, Founder and Director of Rampton Baseley in London

“Mortgage approval levels have been strengthening for much of this year and we’re now seeing this increase in buyer demand start to filter through to actual sales, with monthly transactions being the strongest since 2022. This improving market momentum has also helped to tempt many sellers back into the market who had previously put their plans to move on pause.

“Of course, there will always be a segment of both buyers and sellers who will sit tight in the hopes of some form of property market boost via the upcoming Autumn Budget. However, we’re not seeing this at ground level so much, largely due to the fact that very little has been leaked with regard to the sales sector.”

Marc von Grundherr, Director of Benham and Reeves in London

Regional Trends

Price & Activity Trends

London Trends

Affordability Trends

The first-time buyer monthly mortgage payment is based on Bank of England data of the averages for 90% LTV two-year fixed mortgages from lenders, and the average asking price of a typical first-time buyer home (two bedrooms or fewer) using the Rightmove House Price Index. The equivalent monthly rent is calculated using the same property types (two bedrooms or fewer).

The affordability to buy a first home is based on the Average Weekly Earnings (AWE) dataset from ONS multiplied by 4.5 to get the typical maximum that a person can borrow from a lender. The average asking price of a typical first-time buyer home is taken from the Rightmove House Price Index.

Full Report

Upcoming Dates

18th November

16th December